In West African Economic and Monetary Union (WAEMU), grassroots adoption of virtual assets is growing, appropriate regulation is lagging, and financial risks are piling up.

Somewhere in Dakar, a freelancer is being paid in USDC because her client has no other way to send money across borders cheaply. In Abidjan, a trader is using a P2P platform to convert CFA francs into dollars before an import order. In Cotonou, a family is receiving remittances via a stablecoin wallet because the Western Union fee was simply too high. None of these people are waiting for a regulatory framework before quietly routing their remittances and cross-border payments through innovative gateways, outside the traditional financial system and outside the financial authorities’ perimeter.

In this context, is WAEMU actually ready to regulate virtual assets in a way that protects financial stability and consumers, without stiffling useful innovation?

Clarifying the terms and the perimeter

Any serious discussion on “crypto regulation” in Francophone West Africa has to start by tightening the vocabulary and distinguishing between the various digital instruments circulating in the region. Virtual assets are digital representations of value that can be electronically traded or transferred (primarily cryptocurrencies, stablecoins, and tokenized real-world assets) whereas Central Bank Digital Currencies (CBDCs) are liabilities of the central bank itself. They do not pose the same risks and do not call for the same regulatory treatment.

Internationally, regulators have progressively moved away from technology‑based definitions (“blockchain”, “crypto”) toward activity‑ and risk‑based perimeters: what matters is whether an arrangement enables custody, exchange, issuance, payments, cross‑border transfers, fundraising, or investment management. Within WAEMU, the perimeter must also clearly include virtual asset service providers (VASPs) such as exchanges, custodial wallet providers and certain fintech platforms, which act as gateways between the traditional financial system and decentralised markets. Without this clarification, any future framework risks both overreaching and missing its real targets.

It is also worth distinguishing stablecoins from other crypto assets in the WAEMU context specifically. Unlike Anglophone neighbours where local currency volatility drives crypto adoption as an inflation hedge, the CFA franc’s peg to the Euro makes stablecoins primarily a tool for payment efficiency and remittance cost reduction. This shapes the risk profile: the concern is less hyperinflation arbitrage and more the potential for reduced remittances cost, as well as (to a lesser extent) migration of savings into foreign-denominated instruments, thereby complicating the BCEAO’s reserve management and monetary control.

Current landscape: a growing real‑world usage, in a legal corpus under construction

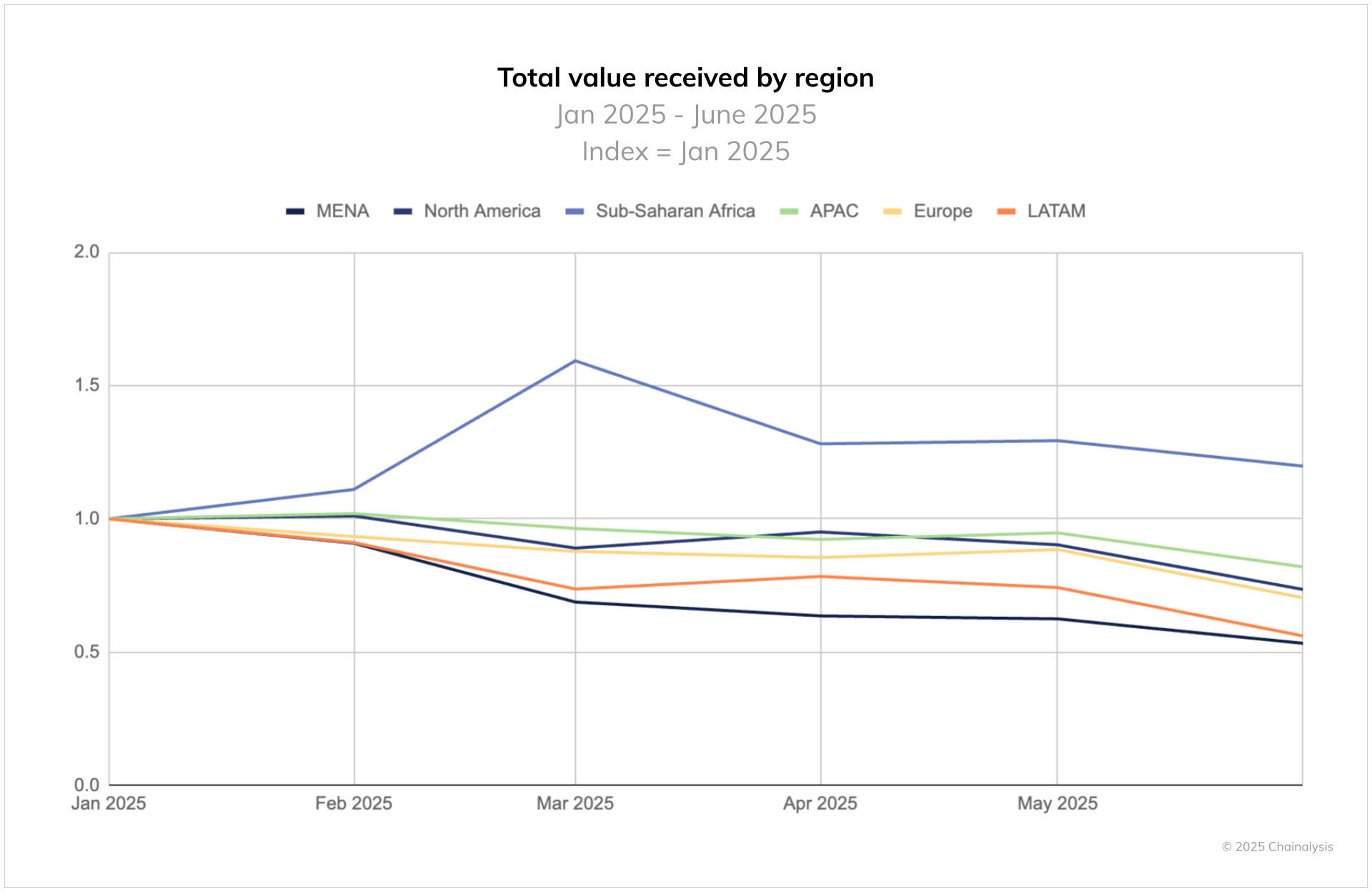

On the ground and from a consumer perspective, crypto adoption is pragmatic more than ideological. Sub‑Saharan Africa has become one of the fastest‑growing crypto regions: according to the 2025 Geography of Crypto Report by Chainalysis, Sub-Saharan Africa received over $205 billion in on-chain value between July 2024 and June 2025 (with stablecoins accounting for 43% of that volume), primarily for remittances and cross‑border payments where traditional fees remain high.

In WAEMU, P2P trading, remittance‑like flows and speculative holding dominate, driven by a young, mobile‑first population already comfortable with mobile money. Formal VASPs remain scarce, often operating from abroad while serving local users digitally, and countries like Senegal and Côte d’Ivoire are seeing growing P2P transaction volumes without a local licensing regime to match.

Legally, however, the zone is no longer a complete blank slate: on 31 March 2023, the WAEMU Council of Ministers adopted a uniform AML/CFT law that (1) introduced definitions of virtual assets and virtual asset service providers (VASPs), and (2) subjects VASPs to prior authorisation or registration and brings them within the perimeter of obligated entities, in line with FATF Recommendation 15. The uniform banking law adopted on 16 June 2023 also broadens the supervised entity perimeter to include fintechs and electronic money institutions. Benin and Senegal have already transposed the AML/CFT provisions through, respectively, Law No. 2024-01 of 20 February 2024 (Benin) and Law No. 2024-08 of 14 February 2024 (Senegal).

But essential implementing texts remain absent: who issues VASP licences? Under what operating conditions? With what prudential supervisory framework? Until adequate response is given, platforms operate without formal recognition, users have no recourse in case of fraud, and there are no suspicious transaction reporting obligations specifically covering crypto flows.

A pressure to act and to upgrade regulatory and supervisory capacity

FATF pressure is the most immediate urgency: 3 or 4 countries of the region (between 2024 and 2025, depending on the date of the decision), representing almost half of the region’s GDP, are on the FATF grey list. This which translates directly into higher correspondent banking costs, increased potential for de-risking and reduced investment attractiveness.

At the same time, regional momentum is building: the African Union’s Digital Trade Protocol (adopted February 2024), Nigeria’s Investment and Securities Act (signed March 2025) and Ghana’s VASP Act (Act 1154, December 2025) all point in the same direction. Outside of Africa, the EU’s Markets in Crypto-Assets Regulation (MiCA) has been fully in force since January 2025.

In WAEMU, the foundations must be strengthened first. Supervisors are already stretched by ‘traditional’ priorities: banking and microfinance oversight, AML/CFT compliance, payment systems, and nascent capital market actors. Virtual assets add layers of complexity: decentralised and borderless transactions, opaque offshore structures, and, most importantly, business models that do not map neatly onto existing licensing categories. Indeed, crypto challenges traditional supervisory reflexes. On-chain transactions are borderless, pseudonymous, and data-intensive. Monitoring these activities requires specialised skills and tools, as well as a shift from entity‑based to more activity‑based supervision, which most agencies are only beginning to explore.

So… is the region ready to regulate virtual assets?

The cautious regulatory silence is becoming an increasingly costly choice. Therefore, the answer is most probably a conditional yes, a ‘yes’ that sits at the intersection between grassroots adoption, institutional capacity, and the tightening requirements of international bodies.

On balance, Francophone West Africa is not ready for an ambitious, all‑encompassing regime modelled on (to avoid saying “copy-pasted from”) the most advanced jurisdictions. It is, however, ready for a phased, scoped and risk‑based first step that focuses on the most material activities and gateways. A pragmatic first move could include drafting a light regional strategy that covers:

- a narrow and clear perimeter,

- a tiered licensing,

- full AML/CFT integration,

- consumer protection safeguards

- interoperability and regional coordination.

Be First to Comment